What are Bonds?

5paisa Research Team

Last Updated: 15 Oct, 2024 06:05 PM IST

Content

- What Is a Bond?

- Types of bonds

- How do bonds work?

- How To Invest in Bonds?

- Bond Elements

- Example of How Bonds Work

- How Do Bond Ratings Work?

- How Bonds Are Priced?

- Features of a Bond

- Conclusion

A bond is a type of debt security. Bonds are issued by borrowers to attract capital from investors ready to extend a loan to them for a specific period of time.

When you purchase a bond, you are making a loan to the issuer, which could be a corporate, government, or municipality. In exchange, the issuer agrees to pay you a specific rate of interest throughout the course of the bond's existence and to refund the bond's principal when it "matures," or becomes due, after a predetermined amount of time.

Learn more about what is a bond, its types, and more, in this blog.

What Is a Bond?

Investment bonds are securities in which investors lend money to a company or a government for a set period and receive interest payments in return. Bonds are regarded as I.O.U.s between lenders and borrowers containing details of the loan and the repayment schedule. Since bonds earn fixed payments over their lifetime, they're often referred to as fixed-income investments. Organizations, such as municipalities, governments, and companies, issue bonds to investors. It is common for companies to sell bonds to finance the ongoing operations, new projects, or acquisitions of their businesses. Governments sell bonds to raise funds and supplement their tax revenues.

Types of bonds

Now that you understand the bond meaning in finance and the concept of bond issuers, let’s get into the details of the types of bonds.

Corporate Bonds

They are debt securities issued by firms and sold to investors. Investors receive fixed or variable interest payments at either a fixed or variable interest rate as a return for their capital investment. Upon maturity, the bond's payments cease and the original investment is repaid. Corporate bonds are generally considered to be a safe and conservative investment in the investment hierarchy. To balance out riskier investments such as growth stocks, investors often add corporate bonds to their portfolios.

Government Bonds

These are debt instruments issued by governments to finance their needs and regulate the money supply. These bonds are often used by the government to finance infrastructure development and government spending. As a result, the government will issue bonds and invite investors to invest. When the bond reaches maturity, the government will repay the principal and interest as specified in the contract.

Government bonds in India are generally long-term investments. Typically, these bonds last between 5 and 40 years. Further, government bonds fall into the category of government securities (G-secs). Both state and federal governments can issue government bonds.

Municipal bonds

The state, city, county, and other non-federal government entities issue municipal bonds. As with corporate bonds, municipal bonds fund projects or ventures within a state or city, such as highways and schools.

A municipal bond's interest is tax-free at both the federal and state levels. Thus, high-net-worth investors and retirees seeking tax-free income can invest in them. There are different types of municipal bonds based on their maturity terms. A short-term bond usually matures within one to three years, while a long-term bond can take up to ten years to mature.

Sovereign Gold Bonds

Central governments issue these bonds to investors who want to invest in gold but do not want to store the gold physically. This bond's interest is tax-exempt. Due to its government backing, it is also regarded as a highly secured bond. If an investor wishes to redeem their investment, they can do so after the first five years. The redemption date will only affect the date of interest payments following the redemption.

RBI Bonds

There are many types of bonds to invest in, but RBI Bonds are one of the most profound. RBI Bonds are issued by the Indian government and can be held by Indian citizens. 12 nationalized banks sell RBI bonds, including the Bank of Baroda, Bank of Maharashtra, State Bank of India, Central Bank of India, and Indian Bank.

The maturity term of an RBI bond is 7 years, but one can demand a return at any time. This, however, carries a penalty.

Unlike tax-free bonds and fixed deposit accounts, these bonds provide higher returns, a safer source of funds, and relatively short lock-in periods.

Inflation-linked Bonds

With inflation-linked bonds, coupon payments and face value are less affected by inflation. The principal amount is adjusted according to the inflation rate, and interest payments are calculated accordingly.

Zero-Coupon Bonds

As the name implies, this financial instrument pays no interest. Until the bond matures, the money invested doesn't earn a regular interest rate on the investment. The bond is also called the pure discount bond. An investor receives the face value when the bond matures, along with the annual returns on the principal amount.

Convertible Bonds

Unlike other bonds, this type of bond pays interest and has a face value at maturity but can be converted into stock of the issuing company at a certain point. It combines the features of debt and equity.

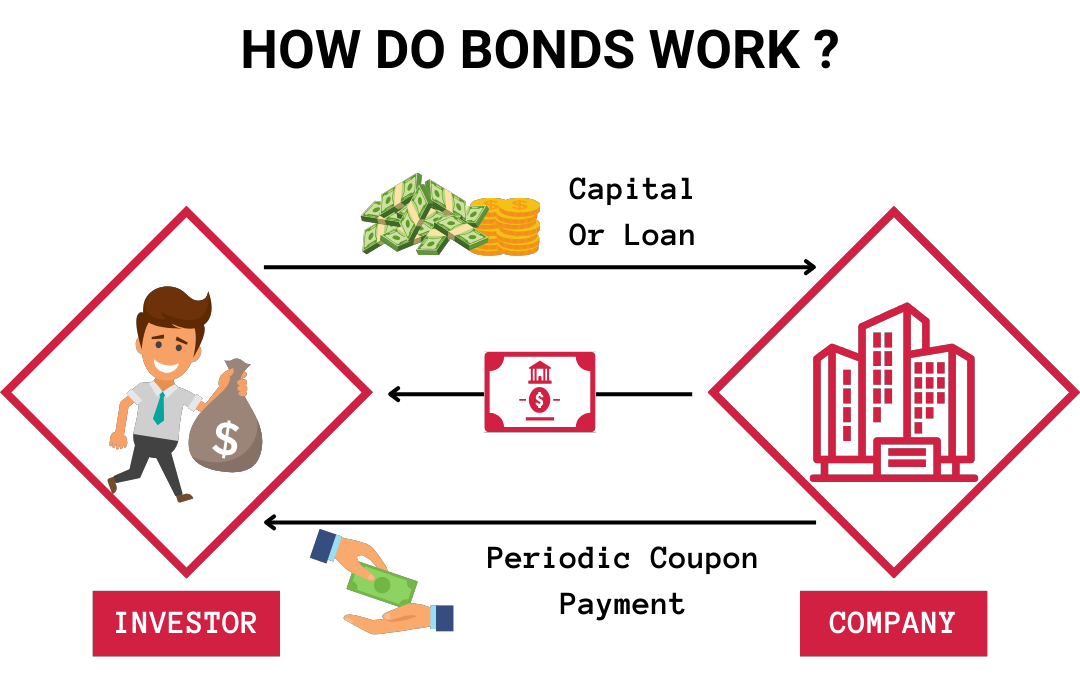

How do bonds work?

Besides stocks (equities) and cash equivalents, bonds are usually considered to be fixed-income debt securities and are one of the most familiar asset classes for individuals.

Whenever a company or other entity needs to raise money to finance a new project, maintain a running operation, or restructure debt, they may issue bonds to investors. To borrow funds (bond principal), the borrower issues a bond that defines the terms of the loan, interest payments, and when the loan must be repaid (maturity date). Bondholders receive interest payments (the coupon) in return for lending their funds to issuers.

Bond prices vary depending on a number of factors, including the credit quality of the issuer, the term of the bond, and the interest rate environment at the time. When the bond matures, the debtor repays the face value, which is the principal.

It is generally possible for the original bondholder to sell the bond to another investor after it has been issued. Therefore, bond investors do not have to hold bonds until they mature.

How To Invest in Bonds?

Bonds may be purchased like stocks through most online and bargain brokers, however there are a few specialty bond brokers. Typically, the federal government sells Treasury bonds and TIPS directly to the public through its TreasuryDirect website. Bonds can also be indirectly purchased by investors through mutual funds or fixed-income exchange-traded funds (ETF). The top online stock brokers are listed on Investopedia, which investors may also check out.

Bond Elements

Investors should familiarize themselves with several aspects of bonds, including

● Issuer: A legal entity that sells securities, such as bonds, to raise money to fund new projects or investments.

● Face value: Also called "par value," this is a price assigned to a stock or bond when it is brought to market by the company. In contrast to market value, face value does not fluctuate. Bonds and stock certificates have a par value printed on them.

● Coupon rate: This is the interest rate on fixed-income security, such as a bond. Bond issuers pay a fixed interest rate based on the face value of their bonds. In most cases, interest is paid semi-annually.

● Issue date: The issue date is when the bond is issued and interest begins to accrue.

● Maturity date: It is the date when your bond's principal will be repaid. Purchasing and selling bonds on the open market is possible before their maturity date. Be aware that the maturity date change will affect the amount of money you receive from the issuer.

● Credit quality: It is the ability and willingness of an issuer to make timely interest and principal payments. A bond's credit rating indicates its quality.

● Market value: A bondholder pays this price when they purchase a bond. What is the difference between this and the face value of your bond? The bond's market value fluctuates, unlike face value. Interest rates and other factors will affect its rise and fall.

● Yield to maturity: A bond's yield to maturity represents the total return you will receive from the date you purchase the bond until it matures.

Example of How Bonds Work

Consider XYZ wants to acquire a large tea company in Asia and wants to borrow INR 100 crore from investors. Based on its market assessment, it believes it can set a coupon rate of 2.5% for its 10-year maturity date. It promises to pay pro-rata interest semi-annually and issues bonds at a par value of INR 1,000. It approaches investors through an investment bank. To raise INR 100 crore, XYZ must sell 10 lakh bonds at INR 1,000 each before paying the fees it would incur.

The interest rate on each INR 1,000 bond is INR 25 per year. Due to the semiannual nature of the interest payment, INR 12.50 will be paid every six months. The INR 1,000 will be returned at the end of 10 years, and the bond will cease to exist if everything goes according to plan.

How Do Bond Ratings Work?

Credit rating firms such as Standard and Poor's, Moody's, and Fitch Ratings provide credit ratings for a company and its bonds. The term "investment grade" refers to the highest caliber bonds, which include those issued by the US government and extremely reliable businesses like several utilities. "High yield" or "junk" bonds are those that are not investment grade but are also not in default. Investors demand a larger coupon payment on these bonds since they have a bigger default risk in the future.

Ratings are created by financial firms using both internal and external variables. The bank's total financial strength rating, a risk indicator that shows how likely it is to need outside financial assistance, is one of the internal criteria. The rating is based on the financial statements and financial statistics of the company being examined.

Networks with other interested parties, such as parent companies, local government organizations, and systematic federal assistance obligations, are examples of additional external impacts. Investigating these parties' creditworthiness is also essential. An extensive external score is determined following the analysis of various external elements. For instance, BBB is the final grade that results from adding this grade to the "intrinsic score."

How Bonds Are Priced?

Bonds are priced based on their specific characteristics. Like any publicly traded security, the bond’s price changes daily depending on supply and demand.

However, bond values follow a logic. Keeping a bond to maturity ensures you'll get your principal plus interest; however, you don't have to hold it to maturity. Bondholders are free to sell their bonds on the open market at any time, where prices may fluctuate, sometimes dramatically.

In the secondary market, bonds are priced based on their face value or par value. Bonds trading above their face value—above par—are said to trade at a premium, while bonds trading below their face value—below par—trade at a discount. Market interest rates and credit ratings play a major role in pricing.

Consider credit ratings: High-rated bonds pay lower coupons (lower fixed interest rates) than low-rated bonds. As a result of the smaller coupon, the bond has a lower yield, which means you get a lower return on investment. Nevertheless, if market demand for your highly rated bond suddenly declines, it will start trading at a discount to par. As a result, its yield would rise, and buyers would earn more over the bond's life because the fixed coupon rate represents a more significant portion of the purchase price.

Market interest rate changes complicate the situation. Bond yields rise along with market interest rates, depressing bond prices as a result. An Indian company, for example, issues bonds for INR 1,000 that carry a 5% coupon. In the following year, interest rates rise, and to keep up with market rates, the same company issues a new bond with a coupon of 5.5%. The new bond would have less demand than the bond with a 5% coupon.

The old 5% bond would trade at a discount, say INR 900, to keep the first bond attractive to investors using the INR 1,000 par example. Investors would receive a discount on the purchase price to make the old bond's yield equivalent to the new 5.5% bond.

Features of a Bond

1. Face Value: The face value of a bond issued by a company represents the cost of a single unit. The terms principal, nominal, or par value can also be used to describe bond prices. After a predetermined amount of time, issuers are required by law to give the investor their money back.

2. Interest or Coupon Rate: Throughout the term of the bond, bonds accrue fixed or variable interest rates that must be paid to creditors on a regular basis. Because interest is traditionally paid on paper bonds in the form of coupons, bond interest rates are also known as coupon rates. Bond interest rates are determined by a number of factors, including bond duration and the issuer's standing in the public debt market.

3. Bond Tenure: The word, or tenure, describes the time frame following bond maturity. These are agreements on financial debt between investors and issuers. An issuer's legal and financial obligations to a creditor or investor are only valid until the end of the term.

4.Credit Quality: The consensus among creditors on the long-term performance of a company's assets is referred to as a bond's credit quality. It is based on how much faith investors have in the bonds of an organization. Bonds are rated by credit rating organizations according to the likelihood that a business would miss payments on its debt.

5. Tradeable Bonds: On the secondary market, bonds may be traded. As a result, ownership may change hands among different investors during a certain period. When market prices surpass the nominal values, these creditors frequently sell their bonds to other organizations so that they may get bonds with higher yields and better credit ratings.

Conclusion

It is important to keep fixed-income investments at the forefront of your investing strategy, regardless of whether you work with a financial professional or manage them yourself. Bonds can provide income and stability as part of a well-diversified investment portfolio.

More About Stock / Share Market

- What is Gap Up and Gap Down in Stock Market Trading?

- What is Nifty ETF?

- ESG Rating or Score - Meaning and Overview

- Tick by Tick Trading: A Complete Overview

- What is Dabba Trading?

- Learn about Sovereign Wealth Fund(SWF)

- Convertible Debentures: A Comprehensive Guide

- CCPS-Compulsory Convertible Preference Shares : Overview

- Order Book and Trade Book: Meaning & Difference

- Tracking Stock: Overview

- Variable Cost

- Fixed Cost

- Green Portfolio

- Spot Market

- QIP(Qualified Institutional Placement)

- Social Stock Exchange(SSE)

- Financial Statements: A Guide for Investors

- Good Till Cancelled

- Emerging Markets Economy

- Difference Between Stock and Share

- Stock Appreciation Rights(SAR)

- Fundamental Analysis in Stocks

- Growth Stocks

- Difference Between ROCE and ROE

- Markеt Mood Index

- Introduction to Fiduciary

- Guerrilla Trading

- E mini Futures

- Contrarian Investing

- What is PEG Ratio

- How to Buy Unlisted Shares?

- Stock Trading

- Clientele Effect

- Fractional Shares

- Cash Dividends

- Liquidating Dividend

- Stock Dividend

- Scrip Dividend

- Property Dividend

- What is a Brokerage Account?

- What is Sub broker?

- How To Become A Sub Broker?

- What is Broking Firm

- What is Support and Resistance in the Stock Market?

- What is DMA in Stock Market?

- Angel Investors

- Sideways Market

- Committee on Uniform Securities Identification Procedures (CUSIP)

- Bottom Line vs Top Line Growth

- Price-to-Book (PB) Ratio

- What is Stock Margin?

- What is NIFTY?

- What is GTT Order (Good Till Triggered)?

- Mandate Amount

- Bond Market

- Market Order vs Limit Order

- Common Stock vs Preferred Stock

- Difference Between Stocks and Bonds

- Difference Between Bonus Share and Stock Split

- What is Nasdaq?

- What is EV EBITDA?

- What is Dow Jones?

- Foreign Exchange Market

- Advance Decline Ratio (ADR)

- F&O Ban

- What are Upper Circuit and Lower Circuit in Share Market

- Over the Counter Market (OTC)

- Cyclical Stock

- Forfeited Shares

- Sweat Equity

- Pivot Points: Meaning, Significance, Uses & Calculation

- SEBI-Registered Investment Advisor

- Pledging of Shares

- Value Investing

- Diluted EPS

- Max Pain

- Outstanding Shares

- What are Long and Short Positions?

- Joint-Stock Company

- What are Common Stocks?

- What is Venture Capital?

- Golden Rules of Accounting

- Primary Market and Secondary Market

- What Is ADR in Stock Market?

- What Is Hedging?

- What are Asset Classes?

- Value Stocks

- Cash Conversion Cycle

- What Is Operating Profit?

- Global Depository Receipts (GDR)

- Block Deal

- What Is Bear Market?

- How to Transfer PF Online?

- Floating Interest Rate

- Debt Market

- Risk Management in stock Market

- PMS Minimum Investment

- Discounted Cash Flow

- Liquidity Trap

- Blue Chip Stocks: Meaning & Features

- Types of Dividend

- What is Stock Market Index?

- What is Retirement Planning?

- What is a Stockbroker?

- What is the Equity Market?

- What is CPR in Trading?

- Technical Analysis of Financial Markets

- Discount Broker

- CE and PE in the Stock Market

- After Market Order

- How to earn ₹1000 per day from the stock market

- Preference Shares

- Share Capital

- Earnings Per Share

- Qualified Institutional Buyers (QIBs)

- What Is the Delisting of Share?

- What Is The ABCD Pattern?

- What is a Contract Note?

- What Are the Types of Investment Banking?

- What are Illiquid stocks?

- What are Perpetual Bonds?

- What is a Deemed Prospectus?

- What is a Freak Trade?

- What is Margin Money?

- What is the Cost of Carry?

- What Are T2T Stocks?

- How to Calculate the Intrinsic Value of a Stock?

- How to Invest in the US Stock Market From India?

- What are NIFTY BeES in India?

- What is Cash Reserve Ratio (CRR)?

- What is Ratio Analysis?

- Preference Shares

- Dividend Yield

- What is Stop Loss in the share market?

- What is an Ex-Dividend Date?

- What is Shorting?

- What is an interim dividend?

- What is Earnings Per Share (EPS)?

- Portfolio Management

- What Is Short Straddle?

- The Intrinsic Value of Shares

- What is Market Capitalization?

- What is ESOP? Features, Benefits & How Do ESOPs Work.

- What is Debt to Equity Ratio?

- What is a stock exchange?

- Capital Markets

- What is EBITDA?

- What is Share Market?

- What is an investment?

- What are Bonds?

- What Is a Budget?

- Portfolio

- Learn How To Calculate The Exponential Moving Average (EMA)

- Everything about the Indian VIX

- The Fundamentals of the Volume in Stock Market

- Offer for Sale (OFS)

- Short Covering Explained

- Efficient Market Hypothesis (EMH): Definition, Forms & Importance

- What Is Sunk Cost: Meaning, Definition, and Examples

- What Is Revenue Expenditure? All You Need To Know

- What are operating expenses?

- Return On Equity (ROE)

- What is FII and DII?

- What is Consumer Price Index (CPI)?

- Blue Chip Companies

- Bad Banks And How They Function.

- The Essence Of Financial Instruments

- How to Calculate Dividend per Share?

- Double Top Pattern

- Double Bottom Pattern

- What is the Buyback of Shares?

- Trend Analysis

- Stock Split

- Right Issue of Shares

- How To Calculate the Valuation of a Company

- Difference between NSE and BSE

- Learn How to Invest in Share Market Online

- How to Select Stocks for Investing

- Do’s and Don’ts of Stock Market Investing for Beginners

- What is Secondary Market?

- What is Disinvestment?

- How to Become Rich in Stock Market

- 6 Tips to Increase your CIBIL Score and Become Loan-worthy

- 7 Top Credit Rating Agencies in India

- Stock Market Crashes In India

- 5 Best Trading Books

- What Is the Taper Tantrum?

- Tax Basics: Section 24 Of The Income Tax Act

- 9 Read-worthy Share Market Books for Novice Investors

- What is Book Value Per Share

- Stop Loss Trigger Price

- Wealth Builder Guide: Difference Between Savings And Investment

- What is Book Value Per Share

- Top Stock Market Investors In India

- Best Low Price Shares to Buy Today

- How Can I Invest in ETF in India?

- What is ETFs in Stocks?

- Best Investment Strategies in Stock Market for Beginners

- How To Analyse Stocks

- Stock Market Basics: How Share Market Works In India

- Bull Market Vs Bear Market

- Treasury Shares: The Secrets Behind The Big Buybacks

- Minimum Investment In Share Market

- What is Delisting of Shares

- Ace Day Trading With Candlestick Charts - Simple Strategy, High Returns

- How Share Price Increase or Decrease

- How to Pick Stocks in Stock Market?

- Ace Intraday Trading With Seven Backtested Tips

- Are You A Growth Investor? Check These Tips to Increase Your Profits

- What Can You Learn From The Warren Buffet Style of Trading

- Value or Growth - Which Investment Style Can be the Best For You?

- Find Why Momentum Investing is Trending Nowadays

- Use Investment Quotes to Improve Your Investment Strategy

- What is Dollar Cost Averaging

- Fundamental Analysis vs Technical Analysis

- Sovereign Gold Bonds

- A Comprehensive Guide To Learn How to Invest In Nifty In India

- What is IOC in Share Market

- Know All About Stop Limit Orders And Use Them To Your Benefit

- What is Scalp Trading?

- What is Paper Trading?

- Difference Between Shares and Debentures

- What is LTP in the Share Market?

- What is Face Value of Share?

- What is PE Ratio?

- What is Primary Market?

- Understanding the Difference between Equity and Preference Shares

- Share Market Basics

- How to Select Stocks for Intraday?

- What is Intraday Trading?

- How Share Market Works In India?

- What are Multibagger Stocks?

- What are Equities?

- What is a Bracket Order?

- What Are Large Cap Stocks?

- A Kickstarter Course: How To Invest In Share Market

- What are Penny Stocks?

- What are Shares?

- What Are Midcap Stocks?

- Beginner's Guide: How to Invest in the Share Market Successfully Read More

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.

Frequently Asked Questions

Throughout its term, bonds earn fixed or variable interest rates that are paid to creditors on a regular basis. Because interest is traditionally paid on paper bonds in the form of coupons, bond interest rates are also known as coupon rates. Bond interest rates are determined by a number of factors, including bond duration and the issuer's standing in the public debt market.

Credit rating firms such as Standard and Poor's, Moody's, and Fitch Ratings provide credit ratings for a company and its bonds. The term "investment grade" refers to the highest caliber bonds, which include those issued by the US government and extremely reliable businesses like several utilities.

"High yield" or "junk" bonds are those that are not investment grade but are also not in default. Investors demand a larger coupon payment on these bonds since they have a bigger default risk in the future.

Anyone who is interested in stable and predictable income and little above the fixed deposited return can make investment in the Bonds.

Government and Municipal bond are considering to be safest bond in India.

Yes, you can make profit from Bonds Investment if you stay holder till it matures.

Yes, the issuer and the Credit rating of the bonds and the market situation ans also the bond is embedded or not.