Truth About Derivatives Turnover

Author - Mr. Prakarsh Gagdani (CEO, 5paisa Capital Ltd)

“Indian Stock Market Turnover is 5X of India’s GDP” read the headline of a top financial newspaper in India. If the attempt was to create sensationalism by using a flawed measure, then they probably have succeeded in gathering the eyeballs. This title is nothing but clickbait!

I’ll tell you why.

Trading turnover especially in the derivative segment, which is often used to gauge the scale of our markets, is deeply flawed and deceptive.

What is Trading turnover?

Trading turnover in simple terms is the product of quantity and price. For example, if you purchase 100 shares of HDFC at a price of ₹2700, your turnover would be ₹2.7 lac. The sum of the values of all trades on the exchanges is known as trading turnover.

The turnover on NSE for 31st March 2023 in the cash segment amounted to ₹55,730 crores, while the equity F&O segment clocked in at an eye-popping ₹123 lakh crores i.e. ₹1.23 trillion. That's a lot of money changing hands in just one day, don't you think?

But here's the catch! There is a fundamental difference in the way turnover is calculated in the cash segment of equity and the derivative segment of equity. In the cash segment, the entire turnover is actual i.e. if you buy and sell 100 shares of HDFC at ₹2700 then the actual turnover is ₹5.4 lakh. But in the derivative segment when it comes to options instrument; more than 90% of the reported turnover is notional and guess what, options as an instrument contribute 90% to the overall turnover in the derivative segment.

What is notional turnover?

Let me explain with an example. Let’s say you buy a single lot of call option on the Nifty with a strike price of ₹17,000 paying a premium of ₹200 per lot size. You only need to put up ₹10,000 i.e. 200 x 50 (lot size of nifty is 50) to do the deal. But wait, the turnover reported for the transaction is ₹8,60,000! That's because the turnover is calculated as strike price plus premium multiplied by the quantity. However, the actual value of the transaction was just ₹10,000.

₹8,60,000 is the notional value of this transaction and ₹10,000 is the premium turnover. As you can see, premium turnover, the money that actually gets traded is just 1.1% of the notional turnover. The bloated turnover you see is because of the way turnover is calculated. So all the fuss about high turnover in Indian capital markets is wrong.

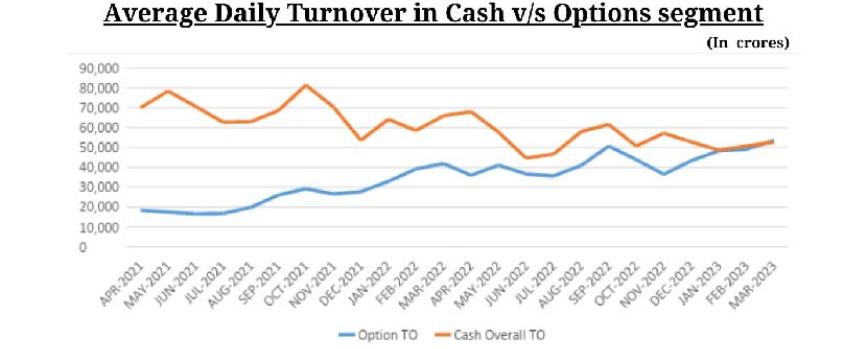

However, this doesn't mean that the Indian capital markets haven't experienced significant growth in recent years. In fact, the number of demat accounts has increased by over 200% between March 2020 - March 2023. And with increased financial savings, growing financial literacy, and the rising popularity of trading among young people, there is a significant growth in the derivative segment. In the last 2 years, the cash turnover has dropped slightly whereas options turnover has more than doubled. Despite this growth, it is nowhere close to the number of ₹12 trillion which is normally reported in the media or otherwise.

Start Investing in 5 mins*

Rs. 20 Flat Per Order | 0% Brokerage