5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

by

5paisa Research Team

6th Jan 2025

Why investors love Varun Beverages Stock

Last Updated: 29th January 2024 - 03:30 pm

Varun Beverages, the PepsiCo franchise bottler in India, has become a favorite among investors. Since the start of the Covid-19 pandemic, its stock has skyrocketed almost 8 times, making it a standout in the fast-moving consumer goods (FMCG) sector.

Well, for those you not aware, it's the company that quenches your thirst with Aquafina water, cools you with drinks like Pepsi, Diet Pepsi, Seven-Up, Mirinda Orange, Mirinda Lemon, Mountain Dew, Seven-Up Nimbooz Masala Soda, Seven-Up. It’s behind the Tropicana juice that charges you up in the morning.

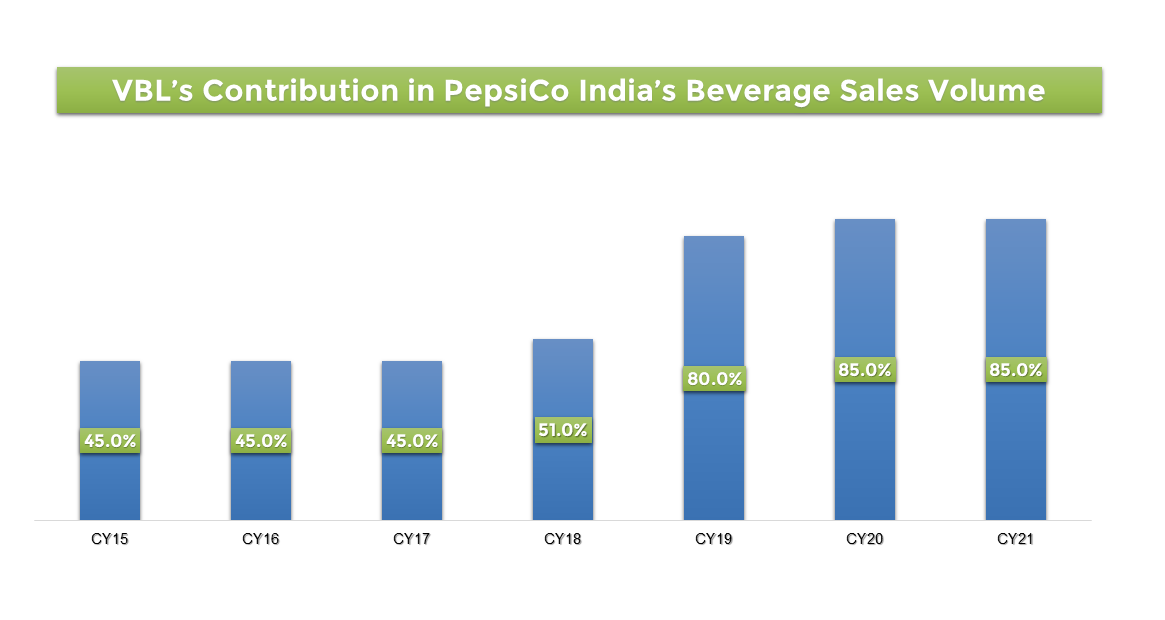

Varun Beverages is the second largest franchisee of PepsiCo (excluding the USA). They produce, distribute, and sell a variety of soft drinks and non-carbonated beverages, including packaged water under PepsiCo trademarks. With franchise rights in 27 states and 7 union territories in India, Varun Beverages covers around 90% of PepsiCo's beverage sales volume in the country. They also hold franchise rights in Nepal, Sri Lanka, Morocco, Zambia, and Zimbabwe.

The company's straightforward business model involves bottling Pepsi Cola, a popular choice among Indians.

They receive the concentrate from PepsiCo, manufacture the drinks, and handle distribution. However, the price of the concentrate, set by PepsiCo, poses a potential risk as Varun Beverages lacks control over it. The concentrate accounts for 10-20% of the company's raw material costs.

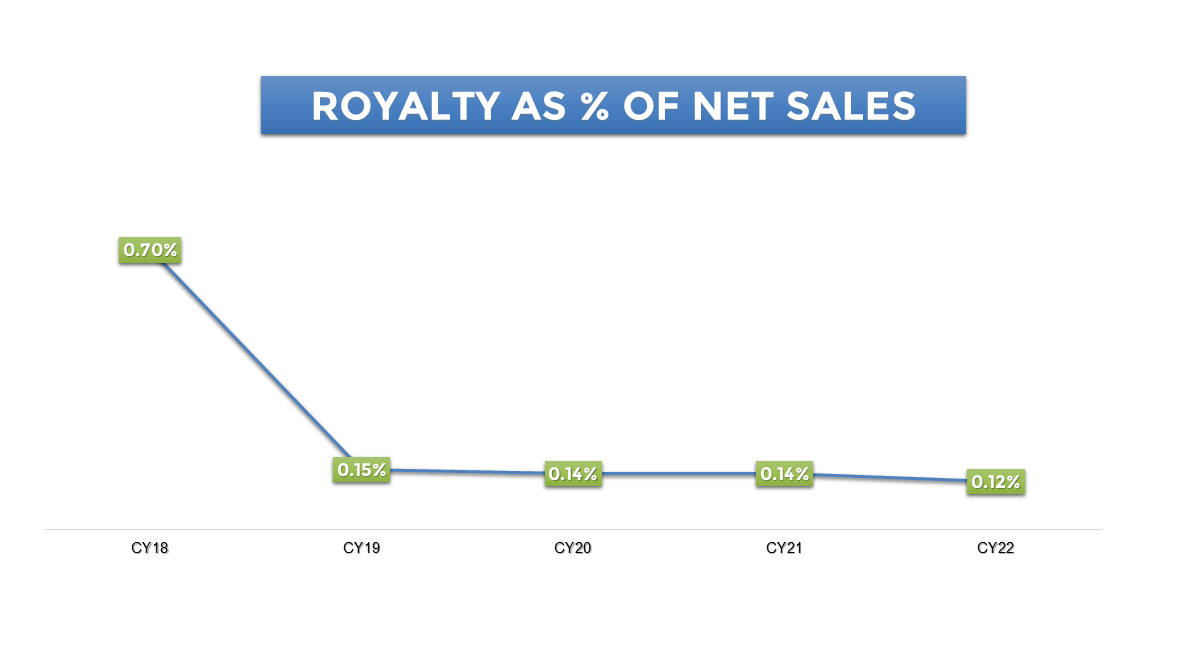

Varun Beverages boasts a unique business approach, managing everything from manufacturing and distribution to warehousing, customer relations, and market execution. PepsiCo provides brands, concentrates, and marketing support, while Varun Beverages takes charge of the manufacturing and supply chain, driving market share growth and cost efficiencies. The company maintains a close partnership with PepsiCo, collaborating on joint projects and strategic planning. Varun Beverages pays a royalty to PepsiCo for using the trademark "LEHAR" with Aquafina and Evervess, subject to potential revisions by PepsiCo.

To enhance operational excellence, Varun Beverages has implemented strategic initiatives like backward integration and centralized raw material sourcing. This includes producing preforms, crowns, plastic closures, corrugated boxes, pads, crates, and shrink-wrap films in certain facilities to ensure efficiency and high-quality standards.

Industry Dynamics:

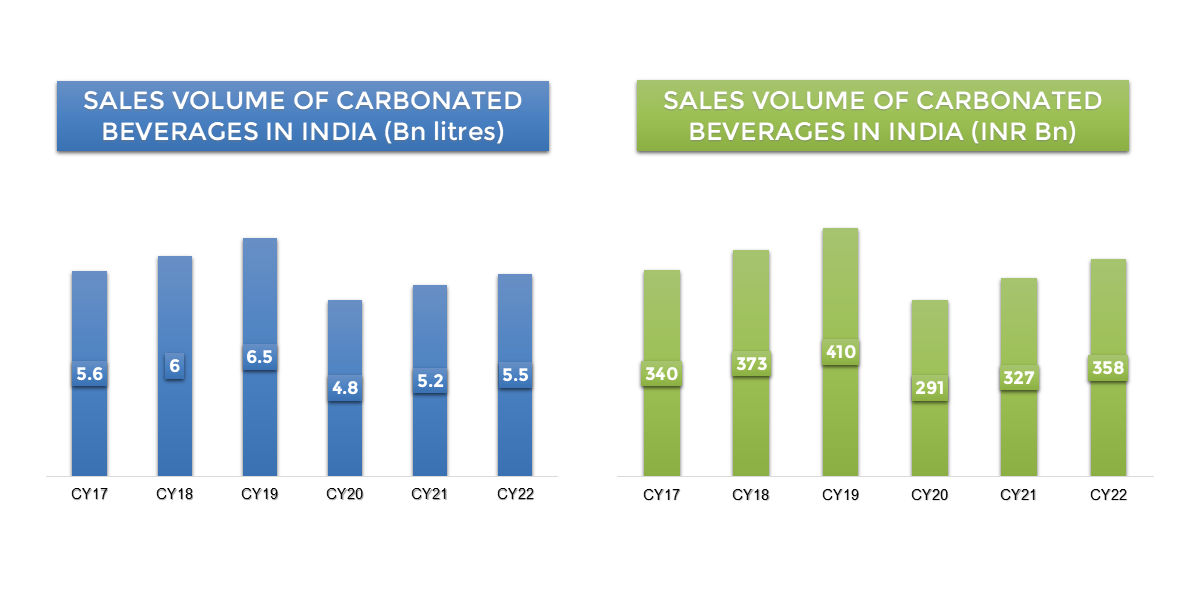

The non-alcoholic beverages market in India is poised for substantial growth, projected to compound at 8.7% and reach ₹1.47 trillion by 2030. Despite the setbacks faced in CY20 and CY21 due to the COVID-19 pandemic, the carbonated drinks market demonstrated resilience, rebounding to 5.5 billion liters in CY22. In terms of value, the sales of carbonated beverages are expected to reach INR 358 billion in CY22. This market is predominantly influenced by major players like Coca-Cola and PepsiCo, boasting a retail volume share of 55.0% and 33.0%, respectively, in CY22.

Globally and within India, the non-alcoholic beverages market exhibits near-duopoly characteristics, with Coca-Cola and PepsiCo controlling a significant majority. The competition between these giants revolves around non-price actions, while small and medium-sized brands, including Parle, contribute to the market diversity.

The industry is undergoing a transformative shift towards healthier beverage options, driven by changing consumer preferences. Additionally, noteworthy events such as the re-launch of the Campa Cola brand under Reliance Industries and the emergence of direct-to-consumer (D2C) startups are expected to shape the market landscape in the coming years.

Market Trends and Growth Drivers:

Several factors contribute to the expected growth in the Indian non-alcoholic beverages market. These include a rise in disposable income, increased rural consumption, higher discretionary spending, evolving consumer preferences, and a substantial young population. The demographic advantage, with a majority of the population aged between 15-64 years and 50% falling under the working age category, positions the industry for increased disposable income.

Varun Beverages' Product Portfolio:

Varun Beverages operates across three key segments:

Carbonated Soft Drinks (CSD): This segment, constituting 70.2% of volumes in CY22 and 72.7% in 9MCY23, includes popular brands licensed by PepsiCo such as Pepsi, Pepsi Black, Mountain Dew, Mirinda, 7UP, Evervess, Duke’s, 7UP Nimbooz Masala Soda, and the energy drink Sting.

Packaged Drinking Water: Accounting for 22.7% of volumes in CY22 and 20.7% in 9MCY23, this segment involves the distribution of PepsiCo-licensed brands Aquafina and Aquavess.

Non-Carbonated Beverages (NCB): Contributing 7.1% of volumes in CY22 and 6.6% in 9MCY23, this segment encompasses diverse beverages licensed by PepsiCo, including Fruit Pulp/Juice-Based Drinks (Tropicana 100%, Tropicana Delight, Slice, and 7UP Nimbooz), Sports drinks (Gatorade), Lipton Iced tea, and ambient temperature Value-added Dairy-based Beverages under CreamBell's license.

In addition to beverages, Varun Beverages is involved in the distribution and sales of PepsiCo's snack brands (Lays, Doritos, and Cheetos) in Morocco and co-manufacturing of Kurkure Puffcorn in India.

Key Drivers of Growth for Varun Beverages Limited (VBL):

Strategic Partnership with PepsiCo:

Varun Beverages Limited (VBL) has fostered a robust partnership with PepsiCo since the 1990s, evolving over two and a half decades. The collaboration has seen expansions in licensed territories, a diversified product portfolio, introduction of various Stock Keeping Units (SKUs), and a widened distribution network.

The symbiotic relationship with PepsiCo involves active development partnerships, joint projects, and a strategic focus. VBL's revenue is intricately tied to PepsiCo, evident in the extended agreement until April 30, 2039.

Market Expansion and Outlet Growth:

VBL has a presence in approximately 3.5 million outlets, out of a total of 12 million FMCG outlets in India, which provides it a huge room for expansion and means there is runway left for it to grow.

It has ambitious plans to annually add 10.0% to 12.0% more outlets, with a focus on those requiring Visi Coolers. The potential improvement in electricity availability in rural India is expected to enhance its market penetration.

Free Cash Flow Generation and Debt Reduction:

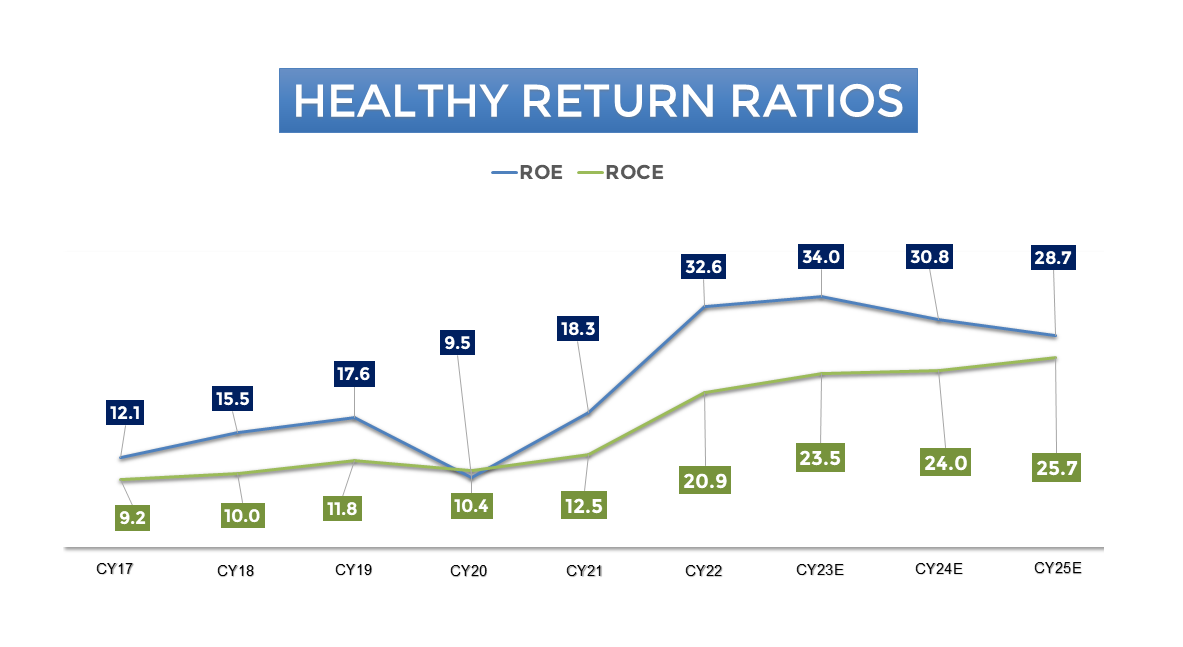

Despite ambitious capital expenditure plans, VBL anticipates robust free cash flow generation. This is likely to support debt reduction, with the company potentially becoming net cash positive by CY25E.

Return on Capital Employed (ROCE) has demonstrated consistent growth, expected to expand by 100-125 basis points annually.

Strategic Capex and Expansion:

The recent acceleration in capital expenditure, particularly in CY21 and CY22, is evident in various projects, including new beverage manufacturing plants, brownfield expansions in international markets, and greenfield facilities in Rajasthan and Madhya Pradesh.

Anticipated capitalization of upcoming projects, including greenfield plants in Uttar Pradesh, Maharashtra, and Odisha, is expected to contribute significantly to revenue potential.

Scouting for More Markets Outside India:

Recognizing limited scope for domestic territory expansion, VBL has taken steps to explore international markets. Wholly-owned subsidiaries in South Africa and Mozambique indicate a strategic move to tap into larger markets with higher per capita consumption.

Ongoing talks with PepsiCo for potential entry into the South African market demonstrate VBL's commitment to geographical expansion and risk mitigation against seasonality.

Diversification into Food Business:

Agreements with PepsiCo for exposure to food businesses in Morocco and the commencement of production and supply of Kurkure Puffcorn in India signify VBL's strategic diversification.

While the beverage market remains a significant opportunity, entry into the foods business positions VBL for potential growth avenues and risk diversification.

Key Risks:

Dependency on PepsiCo:

VBL's entire business model is highly reliant on its strategic relationship with PepsiCo. Any alterations to the franchise agreement, termination, or less favorable renewal terms could adversely impact profitability.

The obligation to allocate a portion of net revenues for PepsiCo and potential changes in this arrangement pose financial risks.

Seasonality Factor:

VBL experiences significant seasonality, with the April-June quarter being the peak season, contributing around 40% of total sales. Expansion into international territories and diversification into the foods business may help mitigate this seasonality risk.

Awareness Towards Healthy Beverages:

Increasing consumer awareness of high sugar content in carbonated soft drinks (CSDs) may lead to a reduction in consumption, affecting volumes. The successful transition towards non-carbonated beverages (NCBs) is crucial for long-term competitiveness.

Regulatory Risks:

The beverage industry is susceptible to regulatory changes related to product content, environmental concerns, and disposal of plastic. Ongoing issues regarding plastic disposal and environmental impact may affect industry operations.

Consumption Pattern Change or Overall Slowdown:

A permanent loss of volumes due to significant changes in consumer preferences or an overall slowdown in the industry presents a risk. External factors such as regulatory changes, higher taxes, and macroeconomic events like the COVID-19 pandemic can impact the industry's discretionary nature.

Financial Performance:

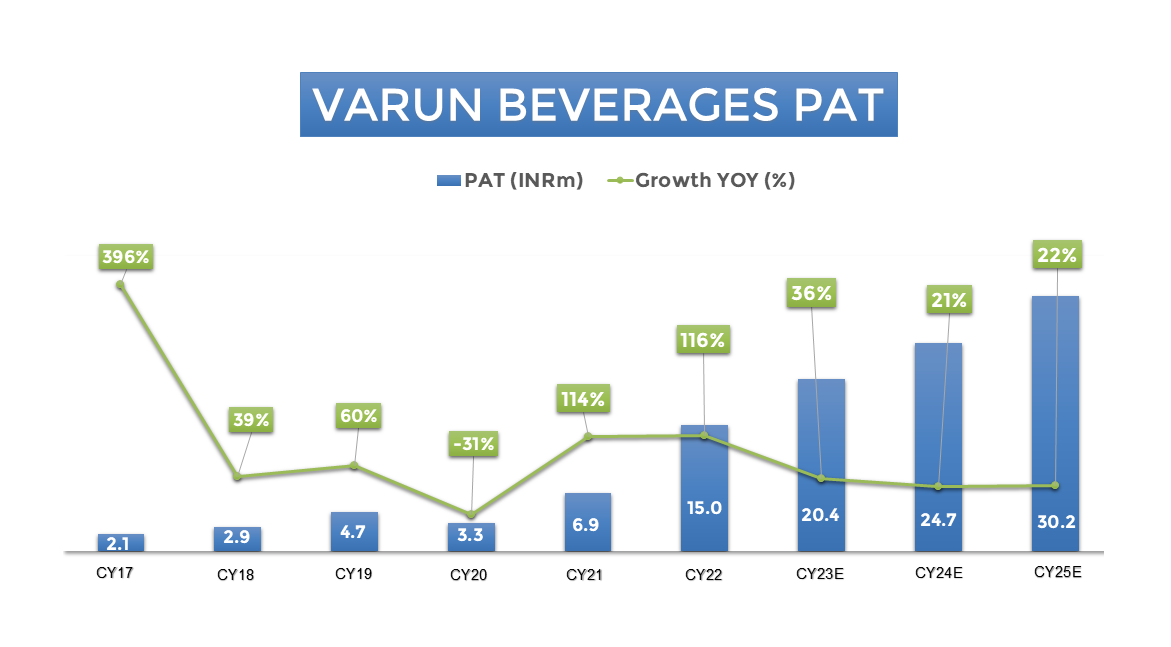

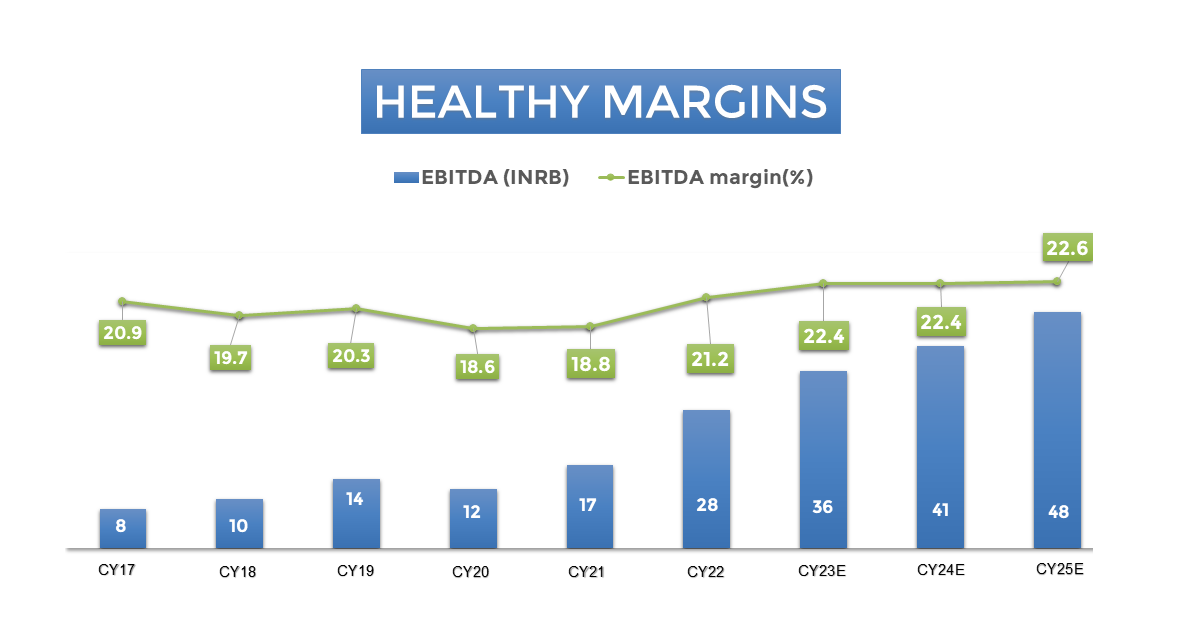

Varun Beverages has demonstrated robust financial performance, with operating revenue growing at a CAGR of 22.7% from INR 7130 crore in 2019 to INR 13173 crore in 2022.

The profit after tax has seen a sharper annualized growth rate of 48.62% in the last three years, reaching INR 1,550 crore.

Notably, the growth in topline and bottomline has been driven by volume increase, operating leverage, and margin improvement, with the change in tax regime contributing to the widening of net profit margins.

FREE Trading & Demat Account

Open FREE Demat Account with endless opportunities.

- Flat ₹20 Brokerage

- Next-gen Trading

- Advance Charting

- Actionable Ideas

Trending on 5paisa

Indian Stock Market Related Articles

Top New Year Stock Picks for 2025: Best Investment Opportunities

by

Sachin Gupta

6th Jan 2025

Top Energy ETFs in India - Best Funds to Invest

by

5paisa Research Team

11th Dec 2024

Top 5 Nifty 50 ETFs in India by Returns

by

5paisa Research Team

11th Dec 2024

Top Multibagger Stocks for the Next 5 Years in India

by

5paisa Research Team

4th Dec 2024

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.