5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

by

5paisa Research Team

6th Jan 2025

Why HDFC bank shares are falling?

Last Updated: 19th January 2024 - 02:19 pm

HDFC Bank, India's largest private sector bank, has witnessed a substantial 11% decline in its share price over the last two days, resulting in a staggering loss of approximately Rs 1.3 lakh crore in market capitalization. This decline is particularly noteworthy as it contributed to more than one-third of the overall Nifty and Sensex downturn, underlining the significance of HDFC Bank's weak performance in the recent market dynamics.

The bank's shares recorded their most challenging trading session since the Covid-induced crash in March 2020, concluding the session with an 8.5% decrease.

This downward trend has raised questions and concerns within the financial community, prompting an exploration of the factors contributing to this notable decline.

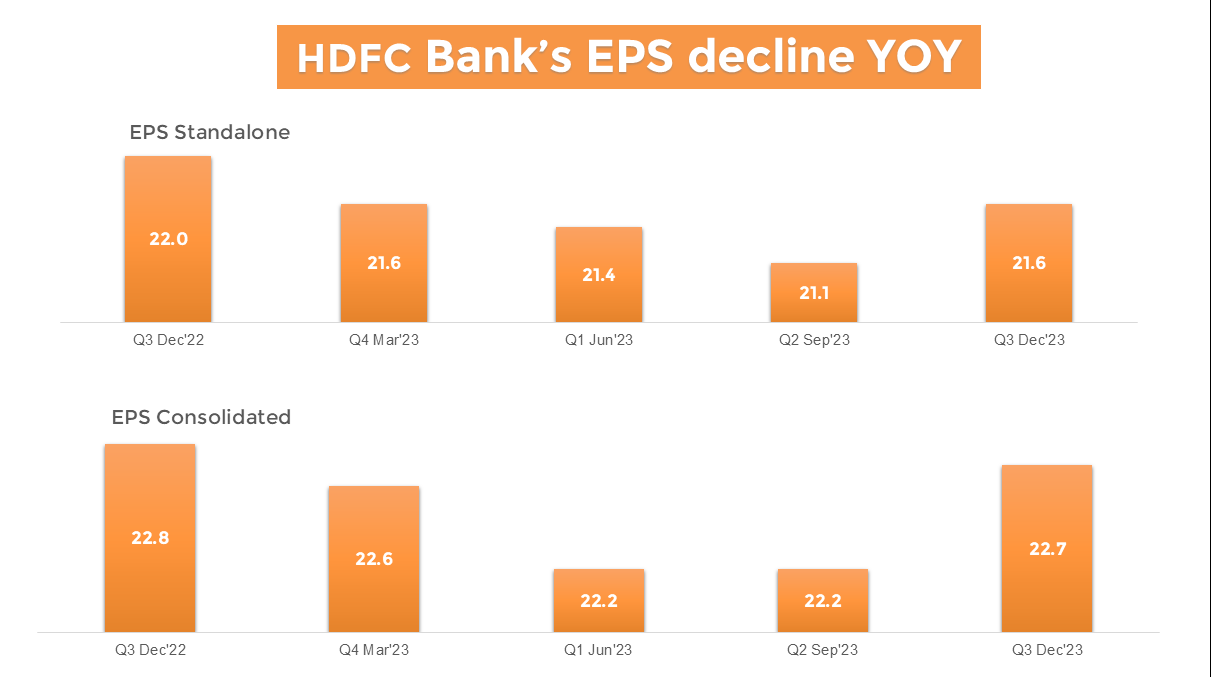

The financial performance of HDFC Bank in the third quarter of FY24 reveals a mixed picture. On the positive side, the bank reported a remarkable standalone net profit growth of 33% year-on-year, reaching ₹16,372 crore. Quarter on quarter, the bank's profit demonstrated a 2.4% increase from ₹15,976 crore in Q2FY24 to ₹16,372 crore in Q3FY24.

However, a closer look at operational metrics reveals areas of concern.

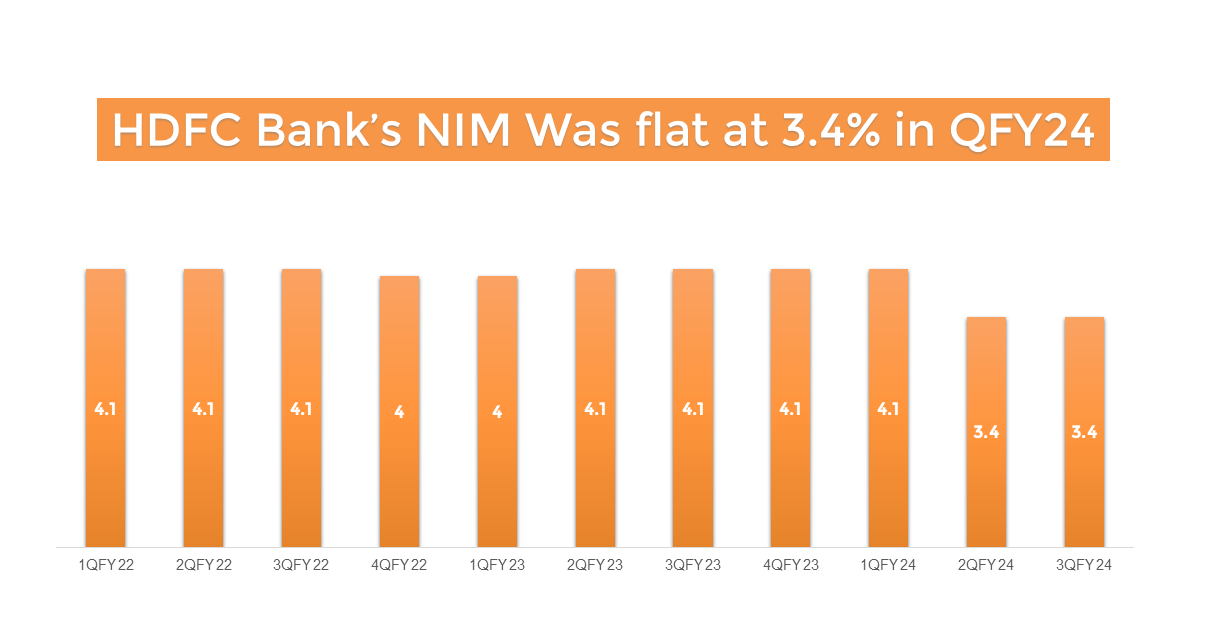

The net interest income (NII) experienced substantial growth, climbing by 23.9% to ₹28,470 crore from the same quarter previous year. However, the net interest income increased by only 4% from the previous quarter, and the net interest margin reported a 3.4% deviation from expectations, standing at 3.56%. The Liquidity Cover Ratio (LCR) dropped from 120% to 109.8% quarter over quarter, indicating a reduction in liquid assets to support loan growth.

Notably, the bank's liquidity in the system turned negative for the first time since 1Q 2020, as revealed by Chief Financial Officer Srinivasan Vaidyanathan in a call with analysts. He emphasized the necessity for deposits to support operational loans, highlighting the central bank's constraints.

HDFC Bank's management acknowledges the deficit in system liquidity as a significant challenge to deposit growth. They anticipate an improvement in the CASA ratio as consumer spending decreases in future quarters.

The loan-to-deposit ratio (LDR) increased from 108.4% to 110.5% quarter over quarter, surpassing the Reserve Bank of India's comfort range of 70-75%. The standalone HDFC Bank's LDR was 89% in Q3FY24, compared to 85% in Q1FY24.

In terms of the loan-to-deposit ratio (LDR), the bank's post-merger LDR reached a tight 110%, exceeding the pre-merger range of 85-89%. The Reserve Bank of India generally favors LDRs between 70-75%, prompting concerns that HDFC Bank, as India's largest private bank, may be setting a precedent with the highest LDR. The loan-to-deposit ratio serves as a key metric for assessing a bank's liquidity by comparing total loans to total deposits. If this ratio is too high, it suggests insufficient liquidity to cover unforeseen fund requirements. Conversely, a low ratio may indicate lower earnings potential.

Investors closely monitor the LDR to ensure adequate liquidity to cover loans, especially in the event of an economic downturn leading to potential defaults. Additionally, the LDR reflects a bank's ability to attract and retain customers, with increasing deposits implying more funds available for lending and potentially higher earnings. While loans are considered assets, deposits represent liabilities, as banks must pay interest on them.

The current scenario has raised concerns among analysts and investors, as heightened levels of credit/deposit (CD) ratio beyond the RBI's comfort range could lead to potential challenges. There are fears that aggressive deposit mobilization or a slowdown in lending growth, or both, may be observed, potentially resulting in margin pressure for banks, including HDFC Bank.

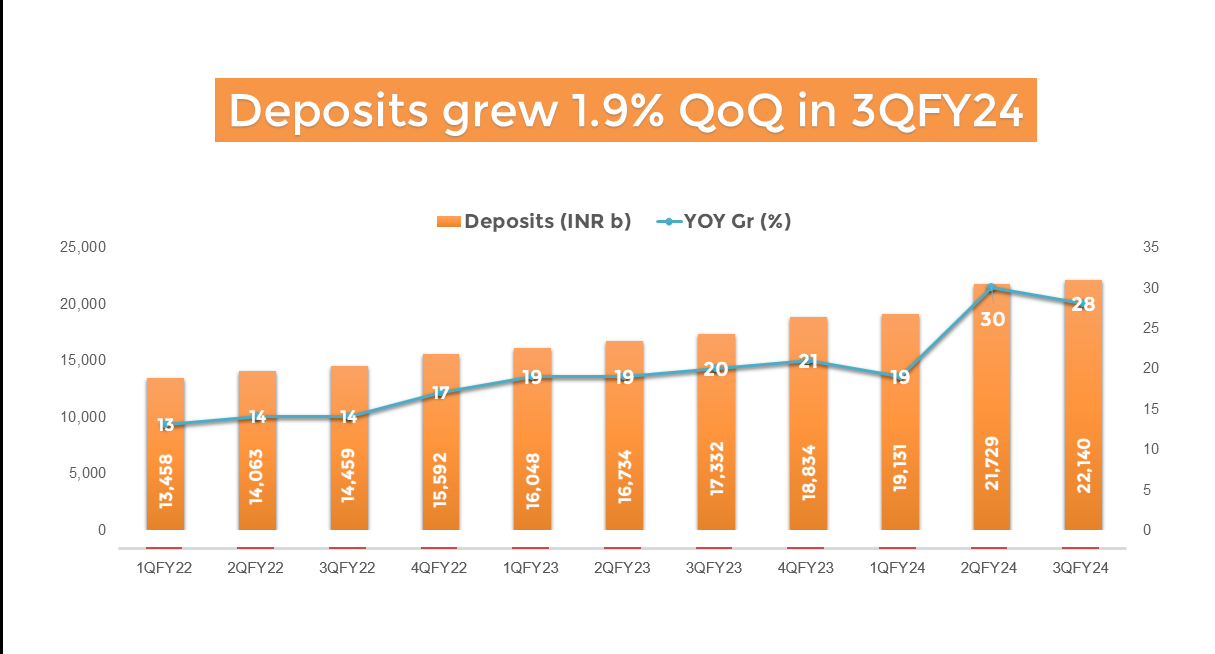

To address the elevated LDR, analysts suggest HDFC Bank needs to grow its deposit growth rate 3-4% higher than its credit growth. In the third quarter, the bank reported gross loan growth of 4.9% sequentially, while deposits grew more modestly at 1.9%. Management indicates plans to restore the balance, but the process is expected to unfold over 3-4 years.

Despite these challenges, the bank's consolidated interest income witnessed an impressive 42% surge to ₹78,008 crore in Q3FY24, up from ₹45,002 crore in Q3FY23. However, concerns arose over the uptick in gross non-performing assets (NPA) to 1.26% from 1.23% the previous year.

In conclusion, HDFC Bank's recent challenges highlight the intricate nature of managing a large private bank in a dynamic economic environment. The intricacies of liquidity, deposit growth, and LDR management require astute decision-making and strategic planning. As the bank navigates through these challenges, the financial community awaits further developments, keenly observing the steps taken by HDFC Bank to restore confidence and maintain its position as a leading player in India's banking sector.

FREE Trading & Demat Account

Open FREE Demat Account with endless opportunities.

- Flat ₹20 Brokerage

- Next-gen Trading

- Advance Charting

- Actionable Ideas

Trending on 5paisa

Indian Stock Market Related Articles

Top New Year Stock Picks for 2025: Best Investment Opportunities

by

Sachin Gupta

6th Jan 2025

Top Energy ETFs in India - Best Funds to Invest

by

5paisa Research Team

11th Dec 2024

Top 5 Nifty 50 ETFs in India by Returns

by

5paisa Research Team

11th Dec 2024

Top Multibagger Stocks for the Next 5 Years in India

by

5paisa Research Team

4th Dec 2024

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.