What Are Option Greeks?

Option Greeks are mathematical measurements that provide valuable insights into the behaviour of options contracts and play a crucial role in making informed investment decisions. In this article, we delve into the concept of Option Greeks in the Indian context, exploring their types, objectives, and important considerations. Let’s unlock the secrets of Delta, Gamma, Vega, Theta, and Rho and equip ourselves with the knowledge to navigate the options market confidently.

Options Greeks: what are they?

Options Greeks are a set of mathematical measurements used to assess the sensitivity of options contracts to changes in various factors. These measurements help traders and investors evaluate their options’ risk and potential profitability. Option Greeks enable market participants to gauge how an option’s price may fluctuate in response to alterations in underlying asset price, time, volatility, interest rates, and other essential variables.

With that information, you can make more informed decisions about which options to trade, and when to trade them.

They are:

Delta– which can help you gauge the likelihood an option will expire in-the-money (ITM), meaning its strike price is below (for calls) or above (for puts) the underlying security’s market price.

Gamma- which can help you estimate how much the Delta might change if the stock price changes.

Theta- which can help you measure how much value an option might lose each day as it approaches expiration.

Vega- which can help you understand how sensitive an option might be to large price swings in the underlying stock.

Rho- which can help you simulates the effect of interest rate changes on an option.

Delta

Delta measures how much an option’s price can be expected to move for every $1 change in the price of the underlying security or index. For example, a Delta of 0.40 means the option’s price will theoretically move $0.40 for every $1 change in the price of the underlying stock or index. As you might guess, this means the higher the Delta, the bigger the price change.

Traders often use Delta to predict whether a given option will expire ITM. So, a Delta of 0.40 is taken to mean that at that moment in time, the option has about a 40% chance of being ITM at expiration. This doesn’t mean higher-Delta options are always profitable. After all, if you paid a large premium for an option that expires ITM, you might not make any money.

You can also think of Delta as the number of shares of the underlying stock the option behaves like. So, a Delta of 0.40 suggests that given a $1 move in the underlying stock, the option will likely gain or lose about the same amount of money as 40 shares of the stock.

Call options-

Call options have a positive Delta that can range from 0.00 to 1.00.

At-the-money options usually have a Delta near 0.50.

The Delta will increase (and approach 1.00) as the option gets deeper ITM.

The Delta of ITM call options will get closer to 1.00 as expiration approaches.

The Delta of out-of-the-money call options will get closer to 0.00 as expiration approaches.

Put options-

Put options have a negative Delta that can range from 0.00 to –1.00.

At-the-money options usually have a Delta near –0.50.

The Delta will decrease (and approach –1.00) as the option gets deeper ITM.

The Delta of ITM put options will get closer to –1.00 as expiration approaches.

The Delta of out-of-the-money put options will get closer to 0.00 as expiration approaches.

Gamma

Gamma (Γ) is a measure of the delta’s change relative to the changes in the price of the underlying asset. If the price of the underlying asset increases by $1, the option’s delta will change by the gamma amount. The main application of gamma is the assessment of the option’s delta.

Formula for Gamma-

Add Formula

Long options have a positive gamma. An option has a maximum gamma when it is at-the-money (option strike price equals the price of the underlying asset). However, gamma decreases when an option is deep-in-the-money or out-the-money.

Theta

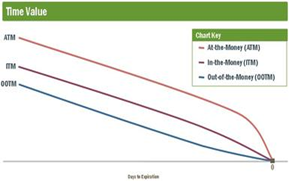

Theta tells you how much the price of an option should decrease each day as the option nears expiration, if all other factors remain the same. This kind of price erosion over time is known as time decay.

Time-value erosion is not linear, meaning the price erosion of at-the-money (ATM), just slightly out-of-the-money, and ITM options generally increases as expiration approaches, while that of far out-of-the-money (OOTM) options generally decreases as expiration approaches.

Vega

Vega measures the rate of change in an option’s price per one-percentage-point change in the implied volatility of the underlying stock. (There’s more on implied volatility below.) While Vega is not a real Greek letter, it is intended to tell you how much an option’s price should move when the volatility of the underlying security or index increases or decreases.

More about Vega-

Volatility is one of the most important factors affecting the value of options.

A drop in Vega will typically cause both calls and puts to lose value.

An increase in Vega will typically cause both calls and puts to gain value.

Neglecting Vega can cause you to potentially overpay when buying options. All other factors being equal, when determining strategy, consider buying options when Vega is below “normal” levels and selling options when Vega is above “normal” levels. One way to determine this is to compare the historical volatility to the implied volatility.

Rho

Rho measures the expected change in an option’s price per one-percentage-point change in interest rates. It tells you how much the price of an option should rise or fall if the risk-free interest rate (U.S. Treasury-bills)* increases or decreases.

More about Rho-

As interest rates increase, the value of call options will generally increase.

As interest rates increase, the value of put options will usually decrease.

For these reasons, call options have positive Rho and put options have negative Rho.

Conclusion

There are four types of options Greeks namely — delta, gamma, theta, and Vega. Each type measures certain factors associated with an options contract such as the fluctuation in the price of the underlying security, the amount of volatility, and time decay of the options contract. Collectively, all four options Greeks allow an options trader to gain insight into their contract and its value.